The statistics of mineral exploration bear out its value proposition. In the great unknown are rich deposits of metals that one can discover, delineate, and sell, or mine to generate profits many 10’s, 100’s or even 1000’s of times greater than the money invested to discover them. Pretty easy but…. the likelihood of success is minimal. We have all heard the tropes 1 in 1000, 5000, 10000 mineralized anomalies will become a mine. I can’t attest to the accuracy of these numbers, but the odds are low in any case. Later in this piece I present a table of assorted discoveries made by ASX listed companies over the last 10 or so years. What becomes self-evident is that even in the best-case scenario of owning a company that makes a discovery and selling it at the very top of its subsequent trading range the returns top out at 50-100 times one’s investment. So….. 1:1000 odds for a 1:100 payout, that’s 10 to 1, or 10c on the dollar. Great if you get lucky (early) but hardly a recipe for success.

The work of Richard Shodde provides some very interesting numbers to analyze. Namely, mineral exploration as a pursuit carries a negative expected return globally! The novice might be surprised to hear this but the seasoned industry participant who has met the many colorful characters that make up the business understand. Moreover, it also becomes clear that the poor discovery rate is the most likely expected outcome given how exploration is funded and conducted.

One might then ask, why would investors keep coming back to exploration when the best outcome over the past 10 years, an investment in Australia yielded a return of 19%. That’s just below 2% per year compounded. Well, most of us are not interested in buying the market, we buy individual stocks and on that front 5, 10, 50 and 100 baggers were not uncommon. This is what everyone is after.

Drawing a parallel with professional gamblers (or advantage players as they are known). All casino games carry a negative expected return, some more negative than others but in all cases negative. This allows casinos to make money. However, in some circumstances such as a skewed distribution of cards in the deck, a particular bonus accumulation on a game, a loss cashback promotion, a clumsy dealer etc., etc. can drive the game into positive return territory. The statistically minded advantage player can in such circumstances pounce and exploit the edge. I draw these parallels intentionally, not because I consider investing in resources or exploration gambling (although one can make it just this) but rather because the popular casino games are ubiquitously understood and can act as useful analogies in describing chance and statistical phenomena.

Mineral exploration success, or discovery, when viewed in the context of individual companies conforms to the statistics of rare events and shares this characterization with other phenomena such as extremely powerful earthquakes or storms that although unlikely, can occur. Despite this, when considering that there are some 800 resources stocks listed on the ASX and assuming that each one is conducting some exploration and testing multiple prospects we are almost guaranteed that even 1 in 100 or 1 in 1000 chance events will happen yearly, even multiple times per year.

Sticking with the casino analogy and viewing all 800 stocks as having the same chance of making a discovery we can imagine a very large roulette wheel with 800 possible outcomes and the number of yearly discoveries being the number of times the wheel is spun. In reality, the situation is more nuanced. Some companies may have too few resources, or alternative priorities to discovery, some might have better geologist and others yet may outspend and out drill their peers. These are all factors affecting the likelihood of a company making a discovery and this complicates our roulette wheel by making the field occupied by some numbers larger than others. How much smaller or larger, that is hard to say but I will explore that idea in the future.

Drawing on our roulette analogy and looping back to the title of the article “Is it possible to predict a mineral discovery?” we can expand on the question by asking “Can we predict a discovery through studying the announcements that precede it and gain an edge in the same way that one could by applying Newtonian physics to predict where a roulette ball will land?”. In my experience the answer is generally no although some cases stick out as yes, yet others carry so little certainty the answer may as well be no.

This poses a further interesting question “As part of an investment strategy should we even consider mineral exploration companies?”.

The final point to unravel before considering real world examples is to consider that not all numbers on our roulette wheel pay the same i.e. not all discoveries are as good as each other.

Discoveries, how good are they and who made them?

Drawing again on Richard Shodde’s work we can observe that across all counted tiers of quality (Tiers) in Australia from 2012 to 2021, 153 discoveries were made and that the collective value of said discoveries was 29.1 billion 2023 dollars or an average value of 190 million per discovery. Now if each of these discoveries was made by a 10 million Market Cap junior that we owned and achieved fair value post-dilution then we would be looking at more or less 153 5 to 10 baggers. If these occurred in sequence, then the effects of compounding would bring even greater returns.

Unfortunately, this is impossible, for many reasons, primary of which is the fact that not all discoveries are material. Don’t get me wrong, if a BHP team found a 50-million-ton Ni-Cu deposit it would be an achievement to be proud of, but unfortunately us lowly punters would have no means of benefiting (other than a possible nearology play). Why? Because the price of BHP would not change. The day BHP announced the mouthwatering intersects from Oak Dam, the price moved up a unimpressive 1.45%. No one cared. It likely moved due to some economic data coming out of China, or the price of Iron ore with which BHP has a high correlation.

For a discovery to be significant as far as we can benefit from it, it must be made by a company that is insignificant. Or better put insignificant considering the discovery made. For example, a company with a sub-5-million-dollar market cap does not have to discover much to move and when it discovers something significant (see ASX:WA1, ASX:PDI) the price runs with its ears pinned back. Moves like these, particularly when you own a lot of stock are like mainlining adrenaline.

So if 27% of all discoveries are made by major companies major companies then we can write these off as something to benefit from. That still leaves 102 discoveries or 10 per year. In addition, a further 105 deposits were discovered by ASX listed companies in the same period outside of Australia. Assuming the same junior/major split that gives us a further 70 discoveries over the period or 17.2 per year. This is a large number of discoveries and presents a significant opportunity to make very nice returns.

If I was ever to make a discovery, I would not tell anyone, but there would be signs.

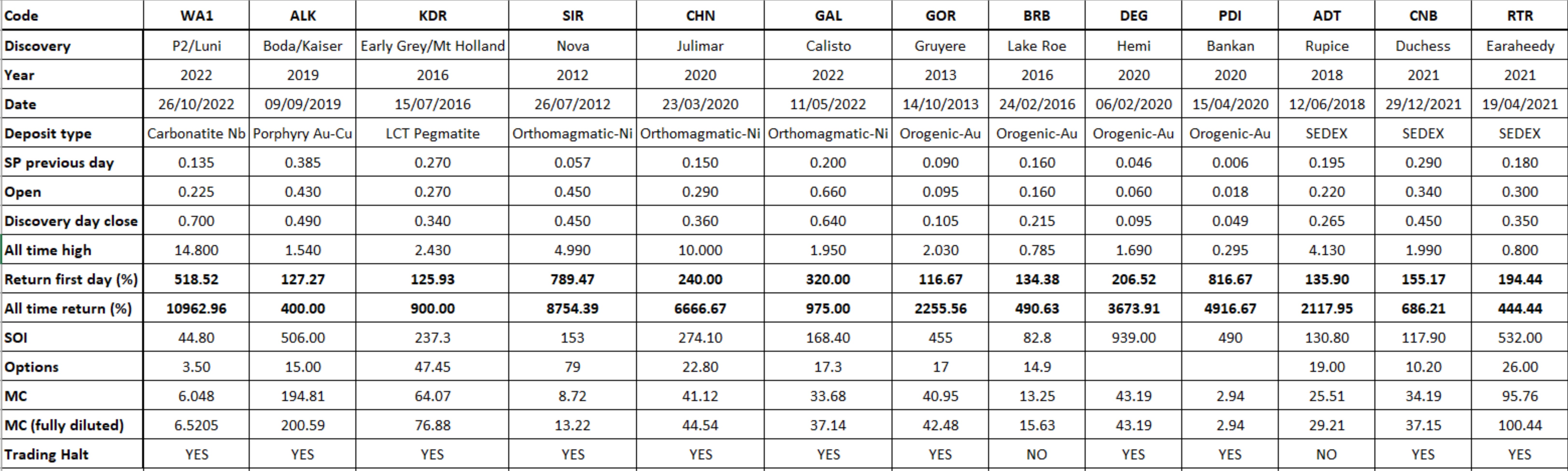

The table below shows selected discoveries made by ASX listed companies from 2012 to 2023. Shown for each are summary statistics as of when I compiled this in early 2024 along with other parameters of interest. I go into a detailed examination of 3 of the examples below. I will do the same for the others in follow up posts and accompany them with geological explanations of the deposits, the typical tools used in their discovery and point out any interesting players in the space I am tracking. We begin with the WA1 discovery.

WA1 Resources- From IOCG’s to Pyrochlore

Disclosure: I bought WA1 on the morning of the discovery and in subsequent days. I have sold out since happy with the returns but maybe I should have held on? Time and metallurgy will tell.

WA1 came straight out of nowhere. Some years prior to their listing I was interested in finding junior resources companies operating way off in remote Greenfields terrains in Australia and one block of tenements that stood out to me was located on the WA/NT border in the West Arunta province owned by a company unfamiliar to me called Tali Resources. The company was privately owned and other than the knowledge that they had pegged some magnetic anomalies in this very remote terrain (along with Encounter Resources) their website provided little other information but for an announcement that the company had entered a farm-in with Rio Tinto where the former would spend some 60 million dollars exploring the package for IOCG’s and orthomagmatic Ni-Cu deposits. Oh well, move on.

WA1 Resources was subsequently floated from a package of tenements that Rio did not seem interested in and the raising was done on the prospect of targeting gravity anomalies for IOCG exploration. The company had a great looking register with executives and Tali owning a large portion of tightly held stock (I generally love this) and they carried on with what one would expect a IOCG explorer to go out and do…. tight gravity surveys and density shell inversions. For those uninitiated this is how geologists target the highest density portions of dense bodies speculated to be related to accumulations of iron-oxides (the IO in IOCG, this presentation gives an account of the method in the Prominent Hill case as an example) that hopefully also contain the copper and gold (CG in IOCG). Three targets emerged and two were subsequently found to be carbonatites, P2 and Luni.

So, could we have predicted the discovery by reading the announcements leading up to the Trading Halt? Absolutely not! I would also go as far as to say that no one in WA1 had any clue what they had until the labs came back. As evidence of this observe the drilling update announcement released on the 18/08/2022 (West Arunta Project Drilling Update). I read this announcement when it came out and thought little of it. The chips looked unimpressive, and the carbonatite intersects were described as:

"exhibiting iron-oxide-carbonate-silicate alteration, with silicified zones often associated with sulphide"

The company subsequently announced that they were flying an EM survey to locate zones of anomalous conductivity, a pursuit not useful or at least typical for carbonatite exploration.

Once the assays came back IOCG’s were never mentioned nor was there any EM conducted again. Niobium was the word from now on.

The important takeaway from this is that exploration success is just as often a surprise outcome of a systematic approach as it is the outcome of design. Generalist (and even more so, self-righteous bearded value investors) are uncomfortable with chance and the statistics involved in the proposition and as a result abstain from participating, leaving only a small number of statistically and geologically minded along with hordes of ephemeral degenerate gamblers and speculators. Depending on the occasion I have been known to be all of the above.

So, what to do about the likes of WA1. Well, be fast to learn about the discovery and even faster to buy. My trade was the first to go through at 22.5c. That was the point at which the position was maximally de-risked, and it was all down to being quick, establishing the transformative significance of the discovery and potential scale (I will deal with this in a future piece) and buying!

It is also important to note that the P2 discovery announcement was not all said and done. In effect P2 was not even the real discovery, it was Luni. Not only was it a second Carbonatite but it was indicative of another process that makes carbonatites great… secondary enrichment. Unlike the glacier scraped terranes of the northern hemisphere, the Australian continent preserves millions of years of weathering that is responsible for such wonders as the Iron Ore of the Pilbara, the Bauxite of Cape York and critical to this discussion the concentrated weathered portions of the Mt. Weld REE deposit.

Carbonatites are made up of carbonate minerals that much like limestone very effectively leach away through weathering, but unlike limestones and the marvelous caves, cenotes and sinking rivers that they produce, carbonatites leach away and, in their absence, concentrate every other non-carbonate mineral in the carbonatite. For example, pyrochlore (the main Nb host mineral at Luni). If the fresh carbonatite has a grade of 0.5 % Nb2O5 and is upgraded through weathering by let’s say 10X then the resultant enriched zone will run 5% Nb2O5. That’s money!!! and confirmation of this ultimately led to the re-rate from 1 to 7 dollars. I exited at this point.

A final note on carbonatites. They like other molten rocks fractionate, meaning that the melt evolves forming over time (and percentage of crystallization) 3 main types of rock, Calciocarbonatite, Magnesiocarbonatite and Ferrocarbonatite. Each is characterized by changes in the dominant carbonate mineral, calcite, dolomite and siderite, respectively. This fractionation process also concentrates elements such as REE and Nb and the high-grade orebody shape outlined at Luni likely maps the occurrence of the latter two rock types with supergene enrichment superimposed on top.

Alkane Resources- Porphyry Cu-Au

Disclosure: I did not participate in this one. Given the companies market cap of some 200 million AUD I did not expect the move that transpired.

Alkane has been around for a while. Prior to this discovery I was somewhat familiar with them through a friend’s employment at their gold mine near Tomingley and another more recent employment out of Dubbo to look after the surrounding exploration portfolio.

Alkane is responsible for several discoveries. It is also responsible for spinning out Australian Strategic Metals (ASX:ASM). Unfortunately, this was done post the Boda discovery making it somewhat difficult to work out what proportion of the 3X rise to attribute to Boda and how much of it to the new entities share distribution.

The company has a track record of exploration success through the Tomingley discovery and growth, followed by discovery success at McPhillamys in 2006, and finally the success at Boda and Kaiser in 2019. Even if we attribute all of the post-discovery 3X rise in SP to Boda it very quickly becomes evident that a 200 million MC company is a much worse speculative instrument that a 5-million-dollar minnow. All this is to reiterate the points made earlier in the article before examining the discovery with respect to its predictability.

Alkane acquired the tenements hosting Boda and Kaiser a long time ago. I seem to recall someone at a conference saying in the 90’s. The company referred to the agglomeration of 3 tenements hosting the mineralization as the Northern Molong Porphyry Project (NMPP). The exploration campaign that ultimately discovered the orebodies in late 2019 started some years earlier in late 2016 and was reported as short updates quarterly, and in two larger announcements here and here. The reader should note that the date of the first announcement is the 3rd of April 2017, more than two years since the stated discovery. However, this announcement carries the following statement:

“Further Drill testing of the Boda target has indicated a significant increase in grade to the south and at depth, confirming the extensive gold and copper mineralization. Drill intercepts include:

KSRC021 43m at 0.47 g/t Au and 0.31 % Cu within a broader zone of 130m grading 0.23 g/t Au and 0.18% Cu from 92m.

and

KSRC022 10m grading 0.90g/t Au and 0.11 % Cu within a broader zone of 290 meters grading 0.17 g/t Au and 0.09% Cu from 0m.”

Moreover, the company interpreted these intersects as:

The monzonite intrusive complexes ‘are similar to those hosting the major gold-copper deposits in the Cadia Valley to the south.”

Certainly, the companies report was interesting and encouraging but hardly something one would expect to move the SP. Moreover, many companies have been encouraged by such intersects in the past only to drill around them and get nothing. Many such examples exist in the Maquarie arc, the Cargo and Yoeval porphyry prospects to name a few. For the following two years the company spread its exploration efforts across several projects including some IP and additional drilling preparation at the NMPP. Finally, the company announced a follow-up drilling campaign on the 19th of April 2019 and its completion in the following quarterly stating that the results were being collated. A trading halt followed, and the discovery was announced on 09/09/2019.

One might point to the final statement regarding results collation as evidence of a discovery. Certainly, this could have been the case but given the many instances in which companies do this only to announce poor or unimproved results we can put this thought down to hindsight bias.

To conclude, this discovery despite demonstrating a positive trend and results worth collating did not present any conclusive signs by which it could be predicted. However, the results did indicate that one should watch for news regarding the project given that the ongoing encouragement did improve the odds of success, even if a 3X price rise was the best that one could achieve.

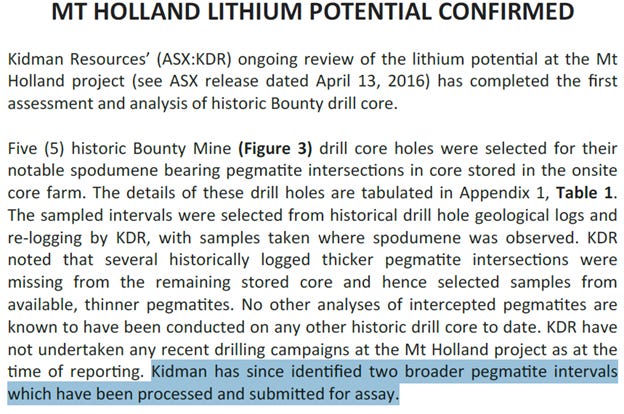

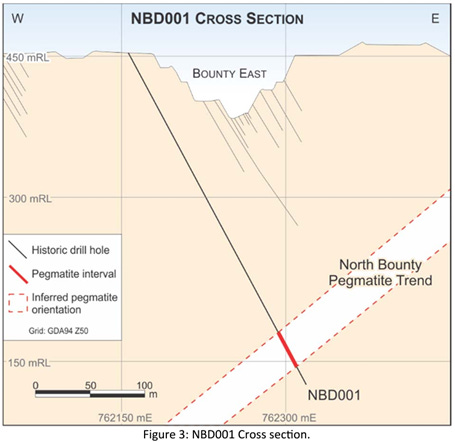

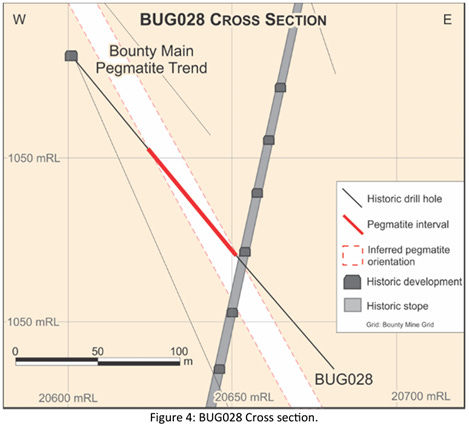

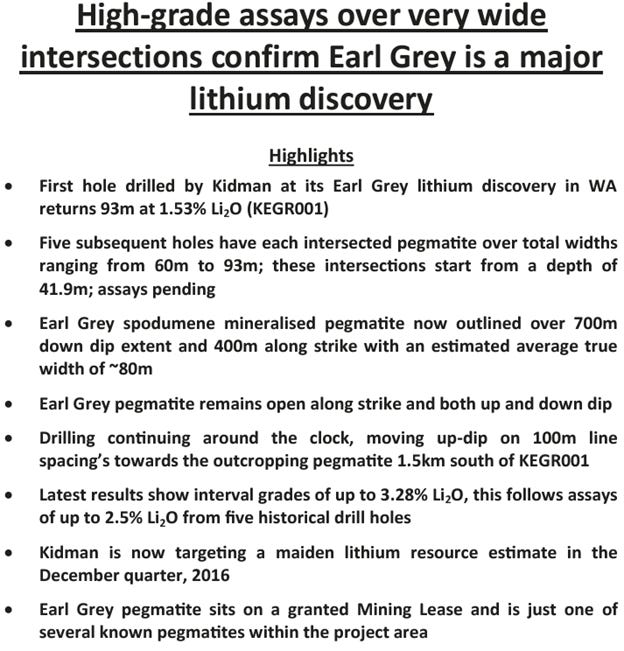

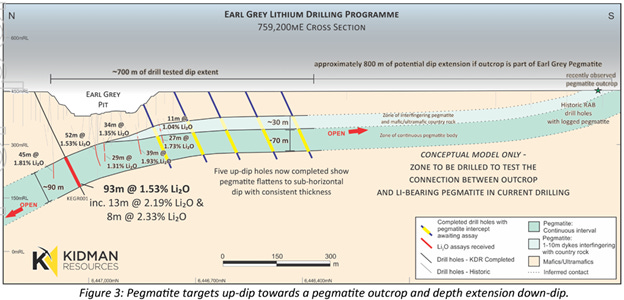

Kidman Resources- New world, new metal, new mine

Disclosure: I was a shareholder of Kidman during this Re-discovery. As per my MO I sold earlier that I should have. The lithium bandwagon is certainly one that I treated with some caution while I continue to question if the electric revolution much like fusion technology will continue to be “in the future”, perhaps perpetually.

When studying this discovery, or better yet re-discovery it is interesting to consider whether the Kidman Resources team acquired the Mt. Holland Au project for its Li or whether they just happened to be at the right place at the right time. Soon after the discovery, questions were raised regarding what their true intentions were. Did they really plan to go after a remnant gold resource or was saying this a tactic to get Mardi metals to cough up the project for a low price. The former certainly felt like they got done dirty and threw a hail Mary Lawsuit at Kidman to get the ground back. The attempt failed. At the end of the day, I am not sure that Kidman was under any obligation to report any intentions to Mardi given the sale process.

Regardless, of the companies sincerity they started talking about lithium after the binding agreement was signed (Mt Holland Project update and Lithium interests) and the company made clear that they had received various solicitations for the lithium interests. Naturally, before agreeing on anything they went out to work out for themselves what they had.

To quote the ever-insightful Rick Rule, before Tesla, BYD and the wider battery trend most miners and explorers spelled “S-P-O-D-U-M-E-N-E” as “W-A-S-T-E”. The Kidman team was dealing with an old core yard at a former gold mine where no pegmatites were assayed but a shitload were logged! For this kind of exploration, one requires a UV light (Spodumene fluoresces) or a handheld LIBS analyzer. The material identified can then be cut and sent to the lab. I don’t know that they used a UV (that’s what I would have done) but they sure did send pegmatites to the lab. Gold miners, particularly pre-2000s assayed material that looked like it carried grade and for Au and Ag. Doing multi-element assays on pegmatites that were clearly unmineralized (with Au) was a waste of money.

While the market was waiting for the assays the company reported some new gold intersects along with the following paragraph here.

Given the expectation of a great discovery, when the assays eventually came back they were “No bueno”: .

The widths were not impressive, but the company did include the highlighted text below.

About 10 days later the company reported what I consider the discovery hole or better yet “discovery assay”:

With a couple of sections:

These looked impressive and made it very clear that those that previously worked at these mines were very familiar with the pegmatites and knew exactly how much spodumene was kicking around. They mined out a section of the pegmatite. The plant would have noticed that along with all the geos on staff. The subsequent announcement made the scale of the discovery clear to visualize.

And it kept getting better:

Kidman went onto raise 21 million dollars for the drill out and to partner with lithium giant SQM. In 2019 Kidman was acquired by Wesfarmers for 776 million dollars thus forming the 50/50 joint venture to develop the mine.

So, could we have predicted the discovery? In my opinion yes. Given the presence of a mine with multiple spodumene intersects the previous employees that worked there would have been very familiar with the presence of spodumene hence the high interest in the Li rights. If one entered the stock early enough one would have had ample opportunity to sell at a profit even if the discovery did not materialize. However, given the abundant core, the old sections, the interest and the lawsuit, one could conclude with a high level of certainty that a discovery would be made.

Conclusions

I hope that the observant reader would have by this point noticed that the discoveries presented here were arranged from least to most predictable. WA1 was a true Greenfields discovery, Boda and Kaiser the product of diligent work and persistence over many years and the Mt. Holland discovery came about through the transformative growth of the lithium market and the likely recollection of spodumene and pegmatites at a long-closed gold mine. Despite this each was an opportunity and could have brought outsize returns, each had its own risk-reward profile, evolution and each one could have been de-risked using various tools available to every speculator or investor (you decide what you are).

On this substack I will continue to publish my examinations of mineral exploration, dissect ideas and assumptions, post-study cases and continue to reveal, describe, and back test strategies. I will also share trading ideas (once I have finished building a position!). All of this is free at the moment, and it may very well continue to be although I reserve the right to change it without notice.

Finally, a repeat of the disclaimer, nothing here is financial advice, comes with no warranty and I take no responsibility for anyone’s financial decisions.

Comments are appreciated

Cheers,

CC

Oh the beauty of youth!

I look forward to your forthcoming articles with eager anticipation.

Not that it's my business to direct your attention in any particular direction or Stock. But I would greatly appreciate your appraisal on TM1 if it's of interest to you. I've Held a considerable sum of these for some time now. There's plenty of interest & banter going on with them presently. HotCopper; 2IC v Hiro? There's no end of Historical, and current info on this ground. I have no qualms in paying for opinions I see value in.

I also Hold decent positions (from my perspective) in AWJ., BC8., BRX., LGM., MEU., STK., TLM., TMS., VTX., YRL., Minor positions in several others. Just to give you an idea of how I play the game.

As I've stated, I have no education in this field. Only 40 plus years in the unforgiving School of Hard Knocks!. I have built a reasonable understanding of what it takes to make an Au & Cu deposit over those years.

I do like the look of RAMP.V., And will watch it closely for an entry. Off last night. You just don't see intersections like that in isolation.

I'm wondering what your age is? I'm a 1957 boy. I've been in this Market since 1983.

So much of what I've now read of your analogies, methodoligies ect., resonate with that of my own. However I do not have your education (Hard Knocks is my schooling). I have made my living as a commercial Bricklayer for more than 45 years. I am now a full time Investor/Speculator (who really knows), and am very happy to avail myself of your Wisdom's for your proposed monthly fee.

Cheers,

Shane