News that caught my eye this week No.4

Gold, Induced polarization anomalies and a couple of PGE targets

In addition to covering some interesting announcements and investment ideas, this week I wanted to put together a survey to get a better idea of what topics readers were most interested in? We’ll start off with that.

Ultimately I plan to write about all these but I may put greater emphasis on certain topics and less on others.

Now the follow ups.

Infini Resources- I88-Fault System & Magnetic Anomalies at Talus Uranium Prospect

The final instalment of near term news the company said they would release following the initial high-uranium soil assays is out. The company promptly went into a Trading Halt for a capital raising as is normally the case for any junior explorer. They take the higher MC and interest to raise cash because in a couple of weeks unless thy can sustaining momentum with better and better announcements interest will wane and they will miss their chance.

The company does make clear that they will hit the ground running in August and expedite all additional soil samples to get more targeting information ahead of drilling that is expected later in the year. The announcement itself and the magnetic high’s the company describes as being potential primary targets are not obvious to me in the absence of another supporting dataset. The company describes needing to find the source of the high uranium and speculates that it could have come from multiple directions. A drill target is not obvious to me here. I see no X marks the spot in the images provided and to a certain extent the company attests to this.

Companies speculations as to the primary source of mineralization

Magnetic map of the area showing a large N-S structure and several interpreted secondary structures.

I am out of this play as a drop in momentum (my expectation), the capital raising and the two gaps on the chart demand more certainty for me to continue to hold. I don’t discount the companies prospect of future discovery and I will keep track of it and return should it materialize.

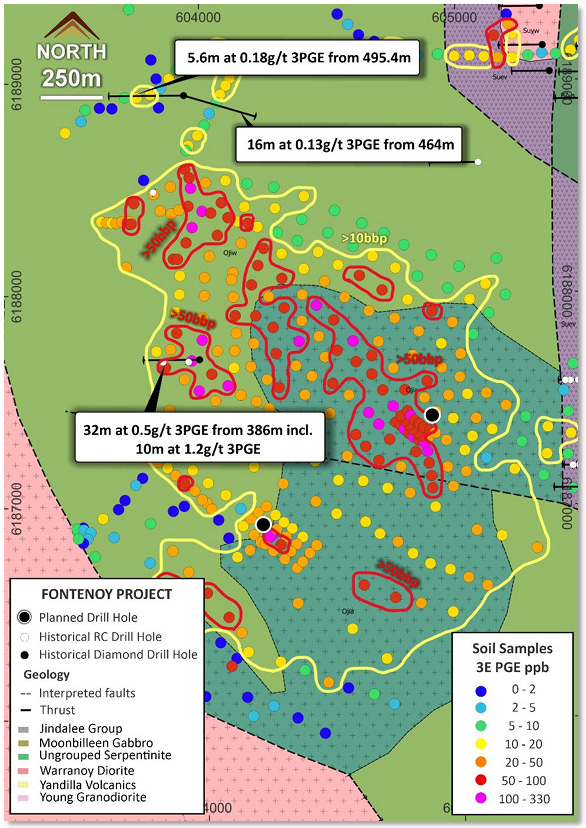

Legacy Minerals-LGM- Drilling Underway Targeting Palladium-Platinum at Fontenoy

The fact that I have included a note on Legacy in every one of these updates so far is not lost on me and I don’t want to give anyone the impression that I am enamored or beguiled with it. I don’t hold any shares, but I do keep track of their announcements, particularly the big targets they are chasing. I definitely did not expect they would drill them all at the same time but that’s what’s happening.

The target being drilled at the moment at Fonetnoy is the product of PGE soil anomalies and likely some “AI”. The JV, or “Alliance partner” on this one is a company called Earth AI. They claim to use “AI” and make bold claims about the effectiveness of their methods. I have strong opinions on this topic that I will cover in the future. Looking at the image below, they are drilling beneath much stronger PGE in-soil anomalies than previously where they came up with broad low grade hits. Given that some out there are predicting a strong future for Pt and Pd, a high-grade discovery could come at just the right time here.

Map of the prospect with locations of drill holes and PGE in soil samples

The commercial arrangements between the two companies are non-standard. I have the original deal announcement here.

New interesting targets

Galileo Mining-GAL- Down Hole EM Survey Identifies Priority Drill Target

Galileo went on a mad dash with their Calisto discovery that I cover in exhaustive detail here:

Is it possible to predict a mineral discovery? Part 1-Nickel Sulphides

Very few announcements get ASX speculators as excited as a credible intersect of a new nickel sulphide system. I have postulated in the past that in the same way the current or perhaps waning generation of speculators would recollect the meteoric rise of Fortescue, Atlas or other Iron Ore stocks a much older, and perhaps first modern generation of resou…

the Callisto discovery was able to demonstrate the prospectivity of the host sills that extend for 10’s of kilometers on the companies tenements. The company also demonstrated that the PGE, Ni and Cu concentrations were largely a factor of sulphide abundance. The majority of the intersects the company made were in disseminated, sometimes heavily disseminated sulphide mineralization with stable sulphide tenor. See the article above for relevant definitions.

So why did this one get my attention? Well, once the poor economics of Calisto became self-evident from the maiden resource and drilling up until that point, the company knew that they needed to explore elsewhere to find something better. This sort of scenario is quite encouraging because the prospectivity of the terrain and the mafic sills has already been proven. All the company has to do now is find the zones of higher sulphide concentrations. Higher than the background mineralization that seems to be present in every part of the sill and higher than Calisto itself. They have lots of space for this.

The shape of the deposit is of a basal accumulation wrapping around a bend in the shape of the sills base. This is caused by the dense sulphide settling to the bottom of the magma chamber or by some local fluid dynamics such as a drop in melt velocity. Once again see the article above for definitions.

Calisto deposit shape occupying the basal position of the mafic sill

The target they have identified from a combination of induced polarization and down hole EM sits 5 km north of and along strike from Calisto. Key thing here is that the target is a large EM plate (200 x 400 m) of significant conductance, about 16000 S. That’s the signature of massive sulphide (or graphite). Key here is that the conductor occupies the same interpreted basal position as Calisto. Provided that the metal tenor stays the same as in the disseminated sulphide, we could be dealing with a deposit of comparable size, i.e. 15-30 million tones, but with an order of magnitude higher grade. Not 2.3 g/t Pd EQ but 10 or 20 g/t Pd EQ. That’s the best case scenario.

Base case it is some barren sulphide either of magmatic or sedimentary origin. Big target that can move the dial for the company. Another Calisto would be of less interest.

Calisto model geological cross-section

Large EM conductor position. Note the apparent similarity to Calisto but with a massive sulphide response.

The company has about 13.6 million in cash and about a 36 million MC.

Strickland Metals-STK- Identification of Large IP Anomaly at Rogozna Project Serbia

When I was thinking about how STK would spend their 60 million courtesy of Northern Star I expected that they would double down on their exploration efforts in WA and maybe even pick up more ground to run even larger Air Core campaigns. Where would WA orogenic Geos be if it was not for AC?!

They did this, but they also decided to acquire the Rogozna project in Serbia. I know a little about this project as a few years ago I was made the offer to work on it which I regretfully passed up. Such is life.

When STK acquired it there was already a 5.4 million oz Au EQ resource on the various skarns that have been defined. These occur at decent open pit grades, near infrastructure and with good strip ratios.

This is one of those projects that will be a mine in my opinion. Most probably a Chinese run mine given Zijin Mining’s very strong presence in the country but a mine none the less. This is what my crystal ball has in store for Strickland. Their sale in a all cash deal with the Rogozna project hosting some future 10 million oz + Au EQ and a spin off of the the Australian assets into some new entity that will keep the Australian Foreign Investment Review Board out of the picture.

Putting the crystal ball gazing aside the results the company has released in this announcement appear to indicate the very near term expansion of resources through new discovery.

Au-As response in soils with existing deposit IP shells and the Obradov Potok (Obrad’s Creek) prospect

Long section demonstrating the association of high IP with existing mineralization and the Obradov Potok response

The results the company has presented require very little speculation and interpretation. If we look at one of the sections the company provided in the original acquisition presentation we can see that the mineralization is made up of a number of porphyry stocks that have intruded into flat carbonate stratigraphy producing Skarns. Deeper down or distally there may be more typical porphyry deposits but very clearly there are multiple stocks and multiple orebodies of which Obradov Potok looks to be another.

STK deposit cross-section

The reason why I highlight this anomaly is because in this sort of near-deposit, poorly explored scenario the expectation from a IP anomaly such as this should not be that it is a false positive but rather that it will be another orebody. In the case of the Rogozna project I am of the opinion that the ounces will stack up fast but that STK will never mine them.

Finally, a repeat of the disclaimer, nothing here is financial advice, comes with no warranty and I take no responsibility for anyone’s financial decisions.

Cheers,

CC

Postscript

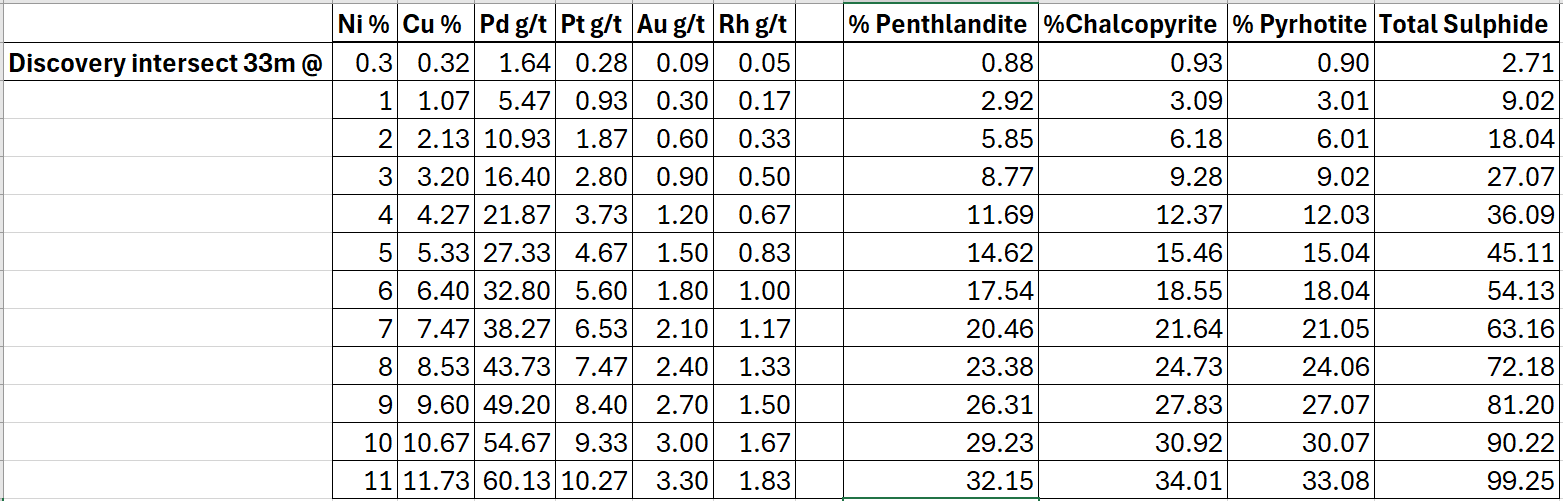

I realized I made the claim that the GAL’s Callisto system would be much higher grade if it occurred with the same metal tenor but as massive sulphide and not 1-5 % disseminated sulphide. The table below takes the original discovery intersect and calculates the grades out to massive sulphide, keeping all the metal relationships the same and assuming that the ratio between Chalcopyrite/Pentlandite/Pyrrhotite to be about 1:1:1.

What becomes quickly self evident is that even approaching massive sulphide at this tenor makes for insane grades. This easily explains the companies very wise exploration rationale and persistence in the area.