Is it possible to predict a mineral discovery? Part 2 Orogenic Gold

These are just as often built as they are discovered

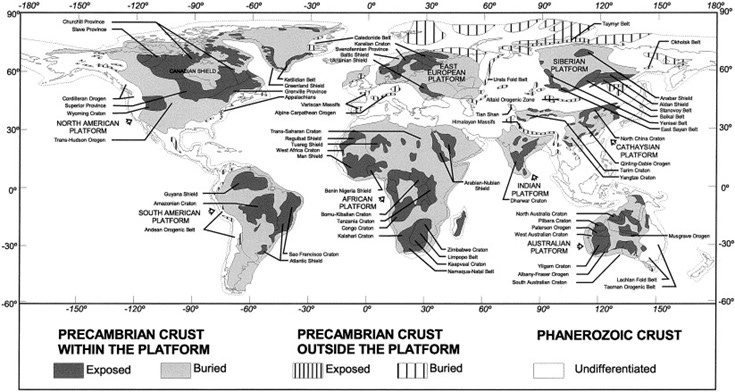

Orogenic Au systems are perhaps the most widely distributed deposit explored for. Speculatively, this is due to their depth of formation and high preservation potential and the fact that the processes that form them have at some point affected masses of crystalline basement in many places. Orogenic deposits occur all over the world and span geological time with cratons or shields being the most prolific producer’s (see map below). Ultimately, these deposits have strong structural and in places lithological controls that result in the formation of high-grade shoots and lower-grade halos making them amenable to both early open pit mining and rapid capital payback and subsequent underground resource definition and ongoing exploitation.

A curious aspect of orogenic discoveries is that they commonly start life as a 1-3 million ounce open pit mines that 20 years latter can have 2 million ounces of underground reserves and a historical production of 7-8 million ounces. This is largely due to their structurally complex nature and the propensity for companies to spend only enough money defining a resource in order to justify the mine investment. This structural complexity can equally lead the investor speculator to many false starts in terms of recognizing a significant discovery. High-grade intersects can be “poddy” or isolated and multiple holes are required to define the extent of the system in some cases. In others conversely, discoveries can be obvious and spectacular. We examine several orogenic deposits here and attempt to answer if their discovery was predictable.

Map Showing the earths cratons/shields from: Orogenic gold and geologic time: a global synthesis

What are orogenic deposits?

A discussion of the nuances of orogenic deposits is beyond the scope of this article, as such I will outline their characteristics in the study cases below only when they are of relevance to answering the underlying question. This will undoubtedly provide a relatively good account of orogenic deposits but for a more detailed account I recommend the paper from which the map above was taken alongside the following presentations.

There are many more on YouTube.

Gold Road Resources- Experts help

Disclosure: I was not actively keeping track of the market at this time and as a result missed out on the discovery.

The story of Gold Road is an interesting example that stands in contrast to the general rule that accountants have no business running exploration companies. Ian Murray despite not having the technical knowledge needed to deliver a discovery nevertheless had the good sense to surround himself with very competent explorers and the strength of character to do what was needed and serve shareholders exceptionally well. More on this later.

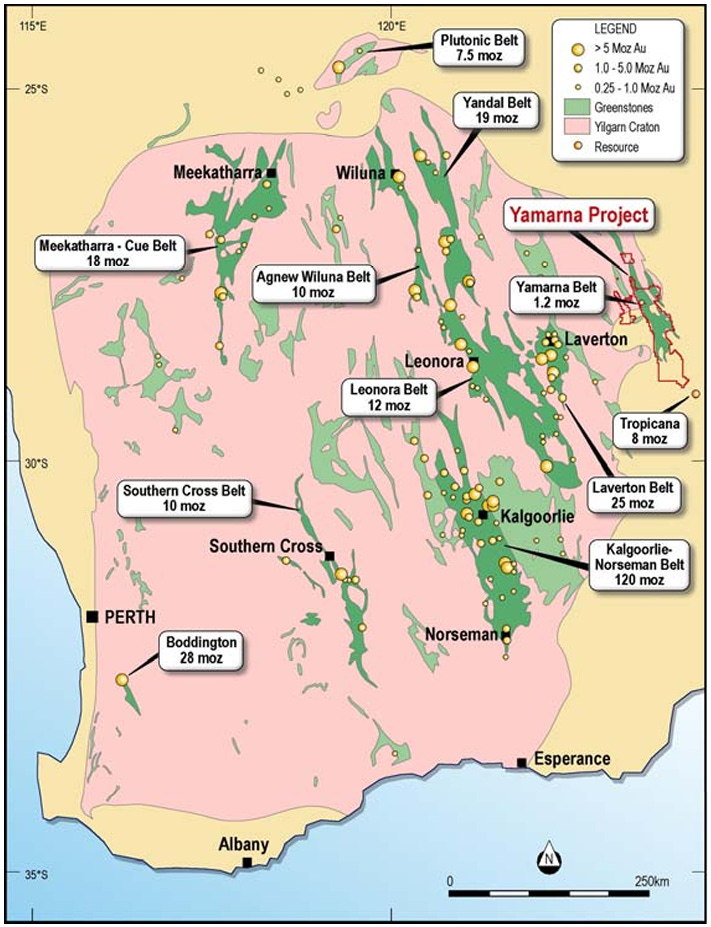

Gold Road’s first success was in consolidating the tenure incorporating a very large portion of the Yamarna belt, that constitutes the farthest eastern reaches of the Yilgarn craton. The Yamarna was known to contain some gold mineralization prior to the Gruyere discovery but unlike many of the other prolific gold terrains of the Yilgarn contained no mines or as far as I am aware historic mines (Fig 2). It was always a little bit too hard. Hard to get to, expensive to explore, transported sand and post-mineral sediment covered (preventing cheap effective geochemical exploration from being effective) and generally ignored as compared to the Kalgoorlie, Leanora, or Laverton belts. A veritable Greenfields terrain of sorts.

Unlike some previous examples we discussed such as that of Sirius or WA1, GOR did not have a sub 5- or 10-million-dollar market cap nor was it completely without resources. Despite trading at near historical lows of some 4.3 cent ahead of the discovery announcement its MC was still some 41 million AUD and it had a small, high-grade resource of some 200k oz at a 8 grams or so. The deposit was nice but small and for the most part drilled out with limited upside. No one was going to take the risk to build a mine this far away. Trucking and toll treatment was not going to cut it either. So, the team had a decision to make, keep drilling a few holes every quarter and keep getting paid till the cash runs out or make the hard decisions and pivot to an uncertain future. Both paths had failure as the most likely outcome, however the choice of pivoting away from Central Bore at least did not guarantee it.

During 2012 the GOR team engaged several of the industry’s best and brightest minds, Jon Hronsky OEM, PGN geosciences and Doug Haynes to review their targeting strategies and shake some of the availability bias that had them exploring around Central Bore for too long. Ultimately, they looked holistically at the entire belt, utilizing the mineral systems approach independently of any previously defined gold anomalism. Aspects such as basin architecture, redox trends and structure were front and center.

Location of Yamarna belt and GOR tenements

The rationale and work are outlined here and pages 15 to 21 of this presentation given at the start of 2013. Both provide a brief account of this work and demonstrate some critical aspects of orogenic deposits and deposit formation in general. Namely, large structures (faults/shear zones) transport large volumes of mineralized fluids. Complex zones along these structures such as bends, kinks and intersections with other faults transport the most fluid and are the focus centers of deposit formation. Critically, observable in GOR’s approach was the recognition that these structures are inherent components of the belt with ample analogues elsewhere in the Yilgarn, and that they are easily discernable in magnetic and gravity data. Interestingly the approach was subsequently detailed in many more presentations (such as this one) post discovery.

Preceding exploration works on these new targets GOR struck a deal with Sumimoto to JV the southern half of their tenements and pursue the northern half on their own (the half that contained Gruyere).

Given that there were so many targets to test the company proceeded with pursuing the cheapest method they could, a company owned and made auger rig. Kyle Prentice describes this process and some of the early successes on this episode of exploration radio that deals with the discovery.

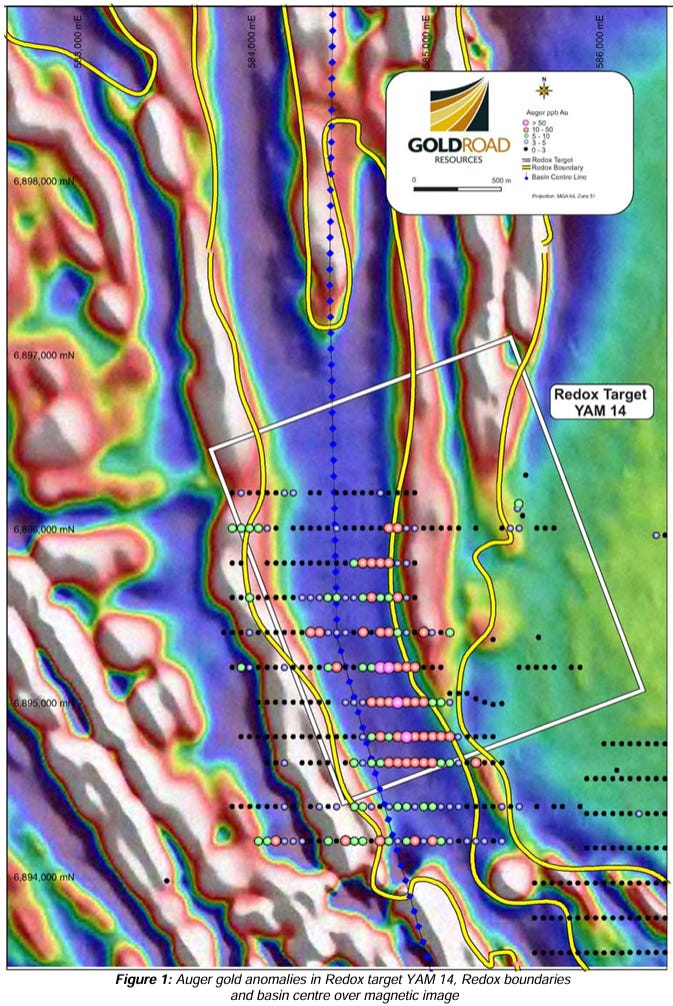

Quickly this method saw encouragement at what was known as the YAM 14 target, outlining a 2 km gold anomaly peaking at 0.22 ppm Au. Hardly an earth-shattering anomaly but nevertheless encouraging. Later it would become apparent that this drilling method was deployed across Gruyere as well but ultimately found to be ineffective and unable to penetrate the overburden and Permian sandstones to reach the orebody.

Auger drilling result over the YAM14 target

Both YAM 14 and Gruyere were subsequently followed up by RAB (Rotary Air Blast) drilling transects and encouragement was first announced from Gruyere and later from YAM 14.

At this point anyone paying attention would have though that YAM 14 was producing much more impressive results and could have been interpreted as being the front runner in becoming a resource. For example, the auger drilling over Gruyere produced near nothing but over YAM 14 it had delivered a coherent anomaly. Similarly, the deeper RAB drilling over YAM 14 produced some interesting intersects and ultimately much higher than the 0.17 ppm Au high observed at Gruyere. Nevertheless, the Gruyere results were much more significant given they were the result of woefully ineffective testing as the company acknowledged.

and

The company carried on for exactly a month with no news from the 09/09 to the 09/10 and hit the market with a trading halt pending exploration results. In the mean-time they announced the hire of a exploration manager, Justin Osbourne, heard in the podcast episode posted above, followed by the discovery announcement.

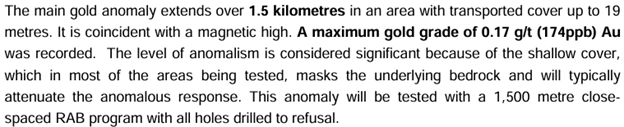

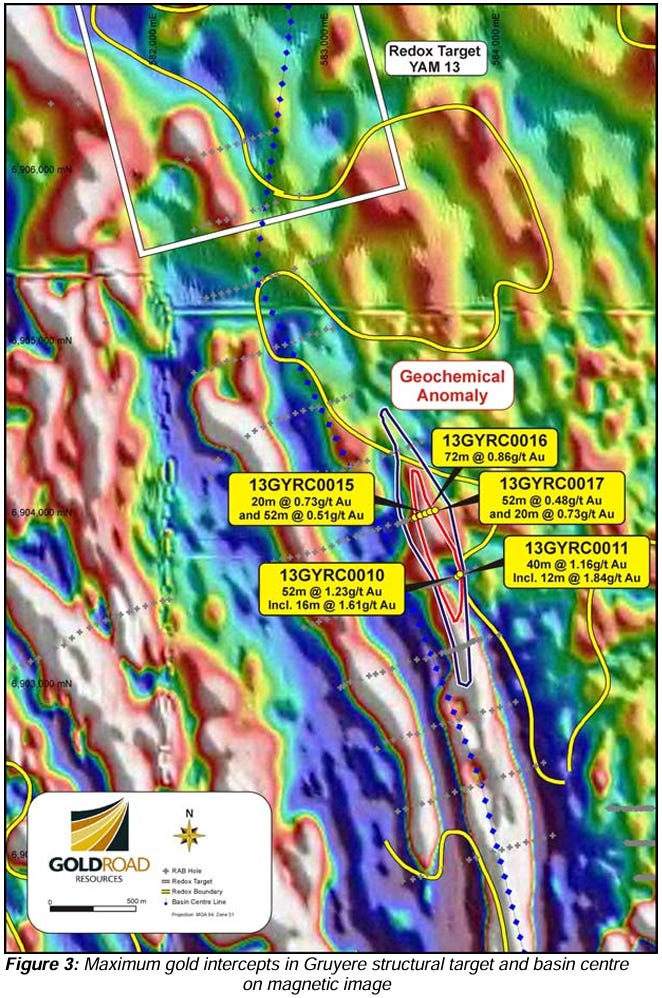

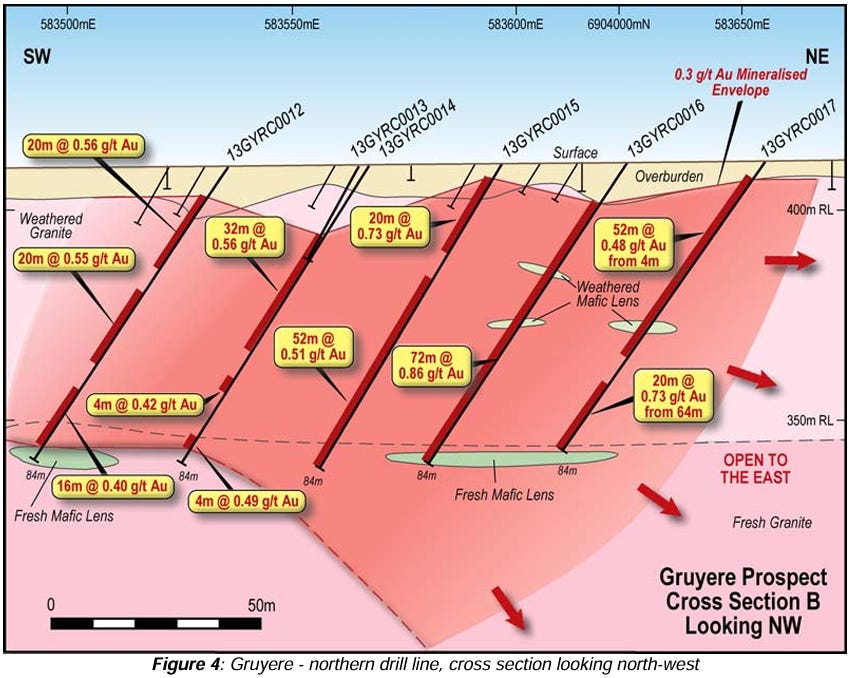

Discovery announcements can be interesting and fickle beasts in that some are not readily recognizable as such and only after further work and supportive evidence is collected can they be considered “the discovery announcement”. This was not the case with Gruyere, it was an obvious discovery. Not only that, looking at it in isolation it was obvious that it would one day be a mine (provided the processing stood up). Why? Simple, it had massive scale, and it was shallow as seen from the cross-sections and maps below. These are very interesting and convey a lot of critical information worth dissecting.

Gruyere discovery plan view

Gruyere discovery cross-section 1

Firstly, looking at the plan map it is obvious that whatever was discovered has a NNW-SSE elongated strike and given the strength and width of the underlying intersects likely occupies the entirety of the Red and possibly Blue geochemical anomalism line. Secondly, the two sections, one spanning 4 and the other 2 holes imply possible continuity and a strike extent of at least 400 meters. Both sections also demonstrate a significant continuity in the mineralization that leave it open in every direction as well as depth. In simple terms, several factors, including the surface anomalism, open mineralization, multiple sections, mineralization being restricted to a distinct intrusive and very wide true width (at this point in-excess of 165m) pointed to a very significant discovery.

Gruyere discovery cross-section 2

Irrespective of one’s ownership of the company pre-discovery, the release of this announcement signaled an obvious buy. From the investor’s perspective, the company was at historical lows and at this price point was a completely de-risked proposition. I will deal with this strategy in a different article, but it is one that I have had much success with.

Was it predictable?

To answer this question here we need to be a bit more specific as to what “it” was? If we define it as zones of gold mineralization then yes, when one is operating in the Yilgarn and led by competent people doing targeted terrain wide exploration, the discovery of some mineralization is to be expected. However, if we define “it” as a near on 10 million oz open pittable deposit then the answer is no. The mineralization at YAM 14 is testament to this. The anomalism was better than that seen at Gruyere and it ended up being caused by the supergene enrichment of rather narrow low-grade mineralized zones. This is not uncommon and represents an important point to recognize, i.e. every geochemical anomaly, no matter how small or weak in the right set of circumstances can be the weak distal manifestation of a great orebody. Under such circumstances one must say that the Gruyere discovery was not predictable but was rather an unlikely outcome of quality exploration work and targeting. The consultants that examined the ground despite being the pinnacle of the sort of quality everyone wants in their exploration campaign still presented GOR with 14 duds and one success. It could of just as easily been 15 duds. I leave it up to the reader to decide if the arithmetic of backing any individual one of these targets in such circumstances works for them.

Gruyere was subsequently drilled out and the company partnered up with AngloGold Ashanti to develop the project. Today exploration is not at the forefront of discussions about the company but rather their production numbers from Gruyere. The genius of this discovery is left to those studying it in the hope of catching the next one.

WIA Gold- The discovery few cared about

Discovery announcement option 1

Discovery announcement option 2

Discovery announcement option 3

Disclosure: I Participated in this discovery and made some money. This one was critical in teaching me the difference (and importance of) commodity Beta to exploration Alpha i.e. a Ok discovery made in a market where sentiment for the metal in question is average to bad will have a substantial impact on the companies share price. The price Alpha driven by the discovery can run into a negative Beta driven by commodity sentiment, or if reversed can make the discovery even more profitable. This is why good discoveries in bad markets will run only when the commodity sentiment changes and why terrible discoveries in hot markets will attain unjustifiable valuations. Had I known this I could have made some real money but now I do!

The first interesting point to make about this discovery is that it was obvious from a technical perspective, about as obvious as one can hope for. I intentionally added three announcements to the start and each one can be considered a discovery announcement depending on what you need to be convinced. The first shows the very strong gold-in-soil anomaly, the second the results of the trenching and the third the first drill holes. The soils were enough for me but as I hope to have demonstrated here, I know enough about this stuff to make educated inferences.

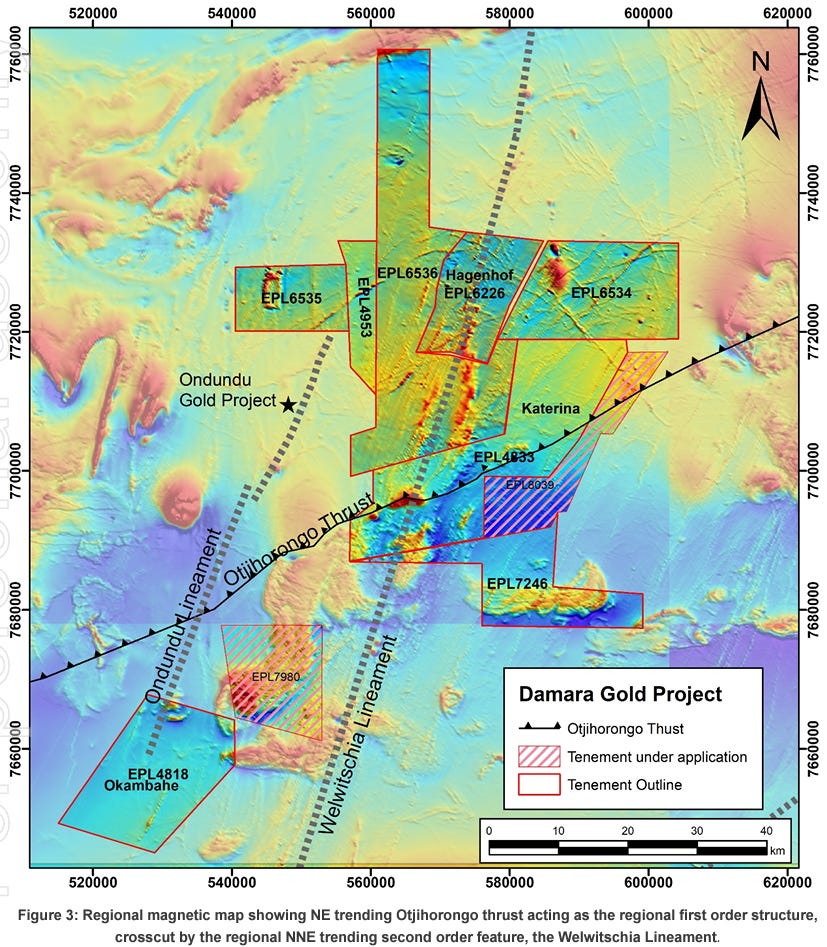

I will dissect this observation but let’s set the stage first. WIA Gold started life as Tanga Resources and under this banner was exploring some sedimentary copper prospects in Namibia. These ultimately disappointed and after a management shake up that brought in several individuals with strong track records and associations with ASX:PDI and the development of the Sukari gold mine in Egypt, they changed their name to WIA gold, raised 7 million dollars and struck a deal with the Namibian government to a large expanded package of tenements they called the Damara gold project shown in the maps below.

The Damara project

The company started to systematically explore the tenements via geochemical soil and stream sediment surveys. I became aware of them at about this time and read the odd announcement released. A company doing this sort of systematic grass-roots exploration in an otherwise unexplored belt was going to pay dividends. The first lot of results were unimpressive as per the map below.

Early soil sampling results

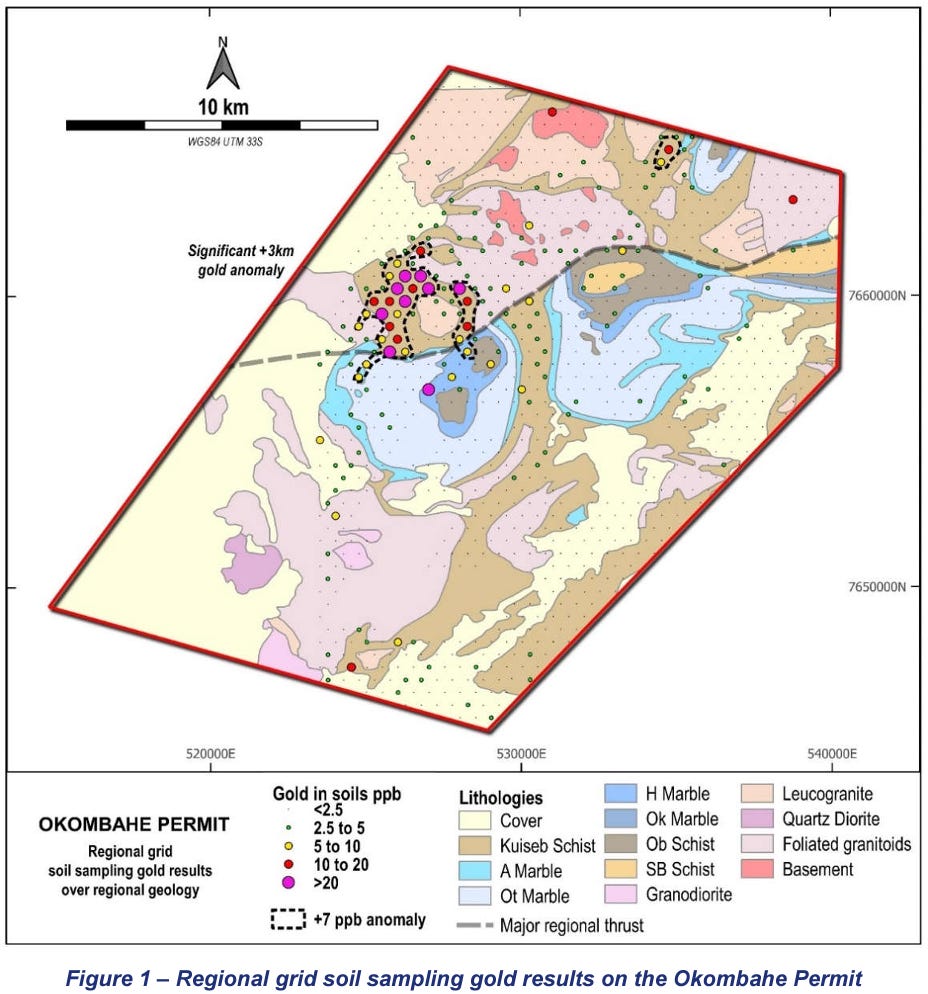

Whereas in the previous discovery discussed, the Gruyere orebody was defined by a auger anomaly of 5 and 10 ppb Au here those anomalies were common and excited no one. Generally such low tenor anomalism is not cause for excitement on tightly spaced sampling grids but when encountered on a wide grid it can be the cause for a follow up. The next lot of result released were extremely exciting.

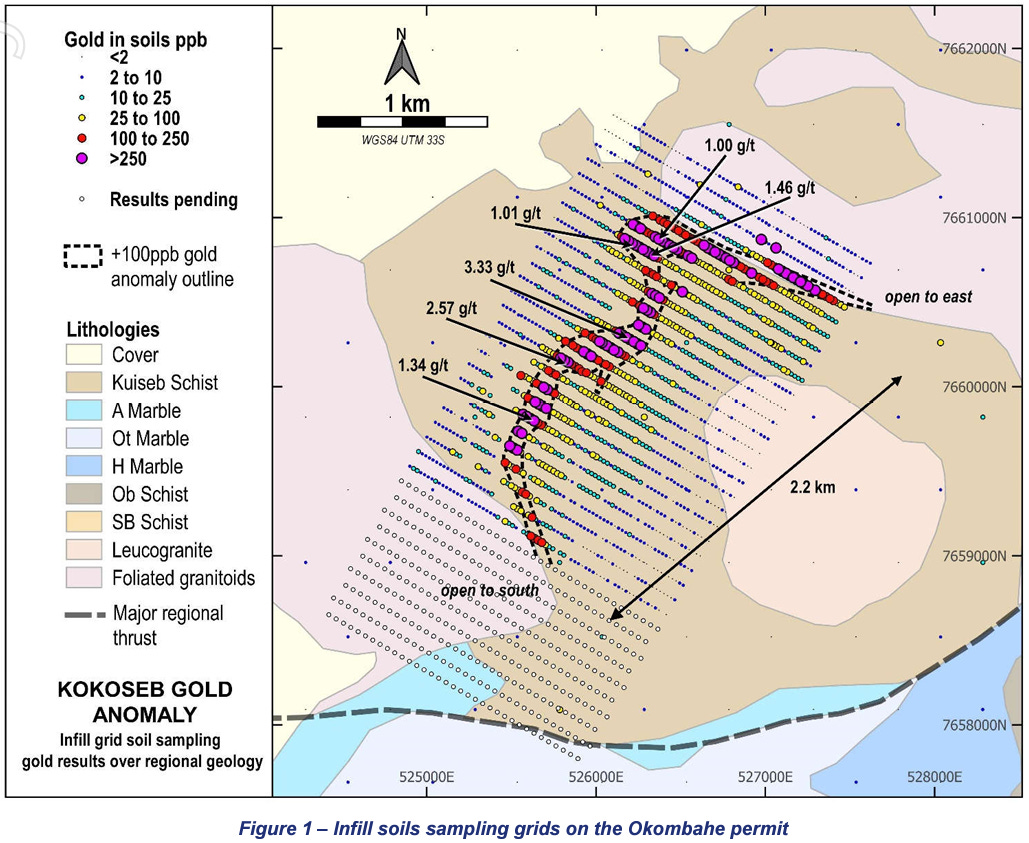

The first map of consequence in this announcement showed the companies 500 x 500 m grid soil sampling over the southernmost tenement where a coherent +20 ppb Au anomaly was centered adjacent to a trust and surrounding a granite and some domes. The anomaly sticks out in its otherwise very low to no Au surroundings.

Early wide spaced indications of a substantial anomaly

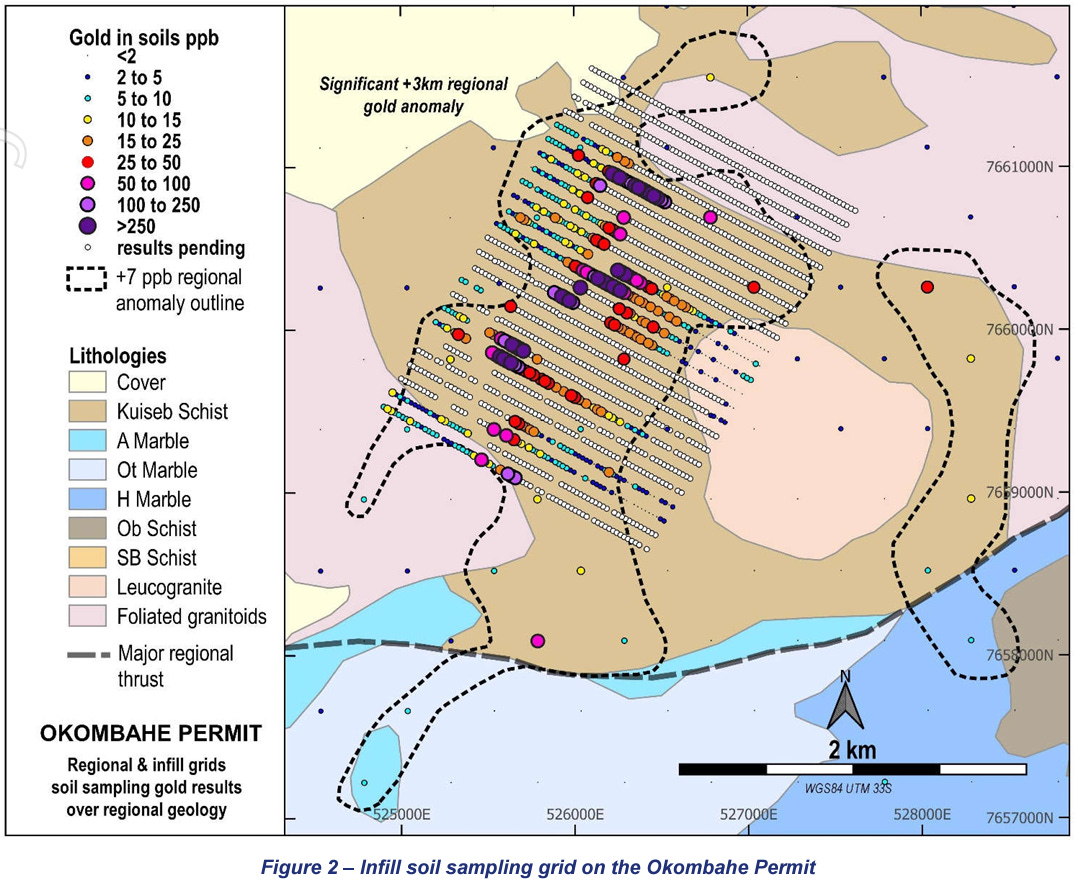

In the same announcement WIA demonstrated the result of its tighter grid soil sampling follow up which effectively discovered the deposit and would eventually outline the shape from which its name was derived, Kokoseb, or Hornbill in the local language. At this point some of the assays from the tighter grid were in from the lab whereas others were still outstanding.

This was the most intense gold in soil anomaly I could find, and I looked damn hard, the closest I came was the Coffee Au deposit anomaly in Canada and even that was smaller in scale and weaker in strength to what WIA had discovered. The anomaly was coherent and looked to define a complex core zone of 250 ppb or 0.25 ppm and above. Normally, this concentration of gold is what one calls ore in large open pit and block cave deposits but here it was the soil. The SP immediately ran from 0.034 to 0.044 cents. An ok result but hardly what I expected as this was an obvious discovery to me.

Tight soil grid revealing the intensity of the anomaly in soils

The announcement subsequently released on the first of November delivered a fuller picture of the anomaly. The SP moved to 8 cents and individual soil samples carried multiple grams of gold. This was unheard of!

The Kokoseb anomaly is the strongest most coherent gold-in-soil anomaly I have ever seen.

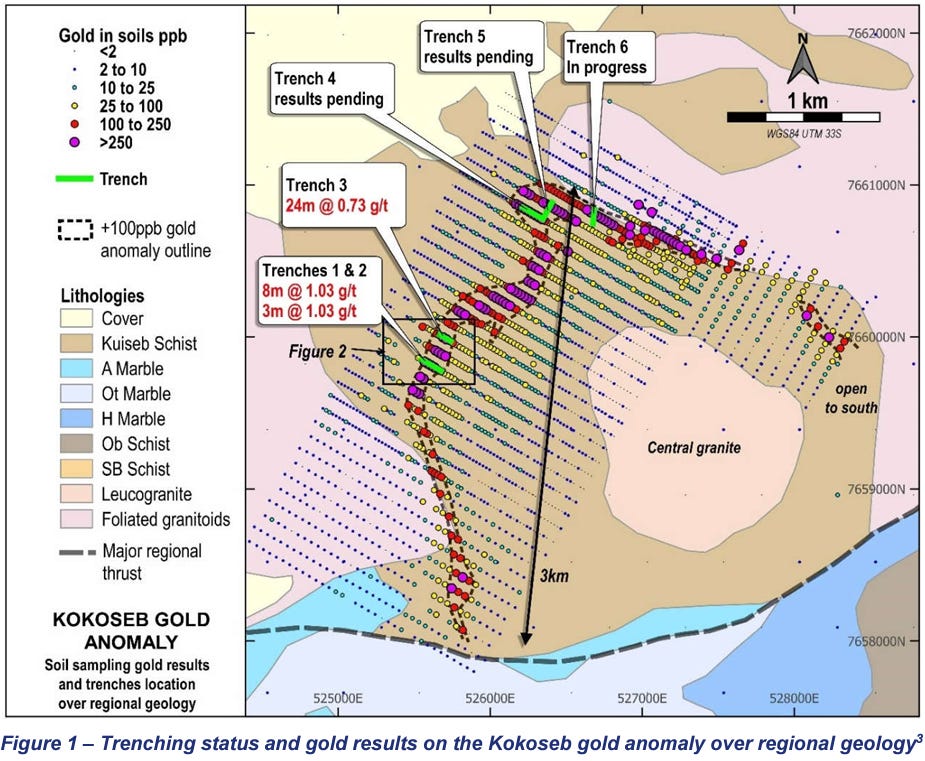

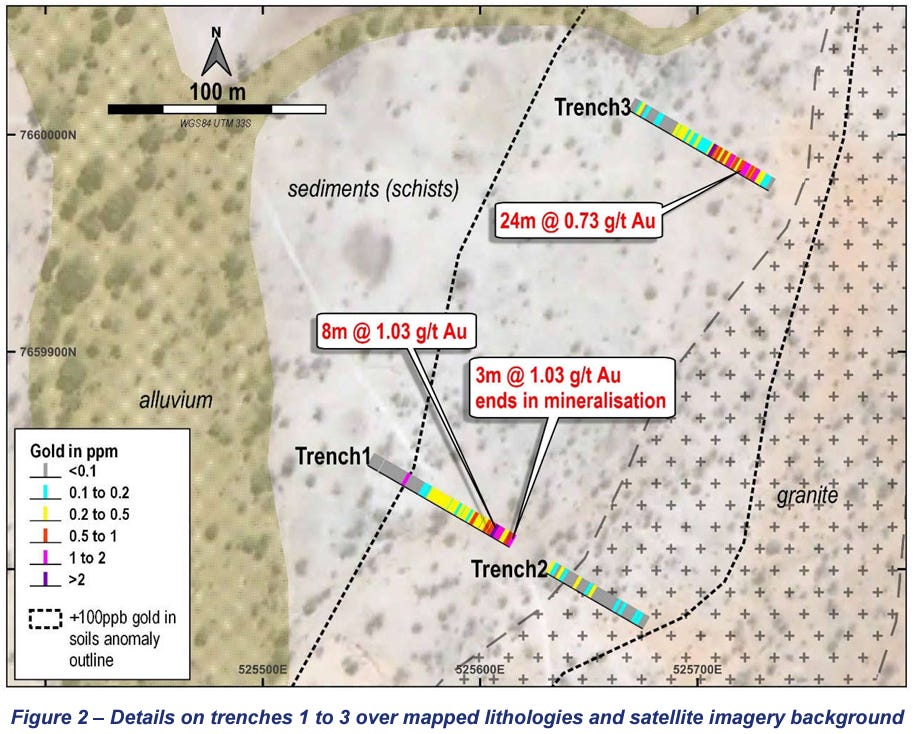

The company continued to expand the anomaly and began to conduct trenching as the mineralization was effectively present under a thin soil veneer and results of 10’s of meters at about 1 ppm started to come in.

Trenching showing bedrock in-situ Au-mineralization

Trenching showing bedrock in-situ Au-mineralization

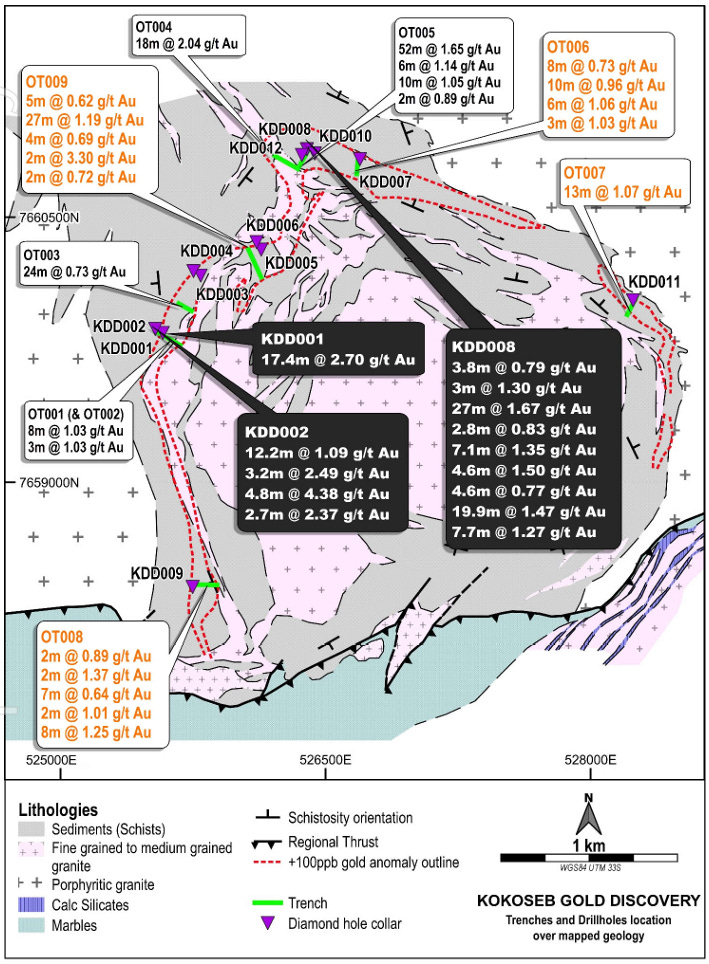

The last thing to do was to drill and take it to the third dimension. As drilling progressed new better trenching results came in and as the first drilling results arrived the company had effectively proven the discovery beyond a doubt.

Several early drill holes showing the strength and consistency of the mineralization across a significant strike extent

The delivery of the first drilling results saw the company rise to some 8.5 cents and then turn around and fall until the following April, reaching a low of 2c. This was inexplicable to me and the reason why this discovery was included in this post. Yes, the strength of the soil anomaly was interesting and the identification of it could have allowed the speculator to buy and make some money but the more interesting question related to why the company, that had just made a discovery of some proportions was seeing its share price fall precipitously whilst at the same time the gold price was rising and the company was delivering intersects that continuously improved. Was it the Lessonde curve? Maybe but they were not approaching production nor were they in a pause of any sort. The decline ultimately stopped with WIA announcing a maiden resource at Kokoseb of 1.3 million ounces or 41 million tones at 1 gram. As the company outlined it went from soil sampling to a maiden resource in under 2 years.

At this point the company had a market cap of 15 million at 2.5 cents and 3.5 million in the bank. It was a bargain by any measure, soon to deliver more ounces and with great metallurgy and in a great jurisdiction, not quite Western Australia but, good none the less. Ultimately, it could have continued to be a bargain, but a transaction involving a nearby Canadian companies undeveloped deposit saw its price run.

Located about 100 km away from Kokoseb, Osino Resources, caught a bid to sell its 3 million oz (81.3 million tones at 1.08 ppm Au) Twin Hills project for an initial bid of 214 million USD to Dundee Precious metals Corporation. As the deal was about to go through Yintai Gold came up and wiped Dundee out with a 272 million dollar bid effectively valuing the Twin Hills deposit, along with a recent two hole discovery at a very high level. In Australian dollar terms this amounted to some 420 million AUD for a deposit that Kokoseb would look like 18 months from now. WIA’s 15-million-dollar MC did not last.

WIA chart since discovery with key events added

Was the discovery predictable?

Absolutely, yes. The only thorn in the equation was the prospect of supergene enrichment being the cause of the soil anomaly i.e. was the underlying mineralization weak and the soils concentrating the gold? This could have overstated the strength of the mineralization, but a rudimentary investigation of the area online would have found an absence of saprolite development and excluded this as a possibility.

This was done in the same way as studying the paleo-climate of the West Arunta to predict an abundance of supergene enriched Nb at Luni, described here:

Is it possible to predict a mineral discovery? The Preamble

The statistics of mineral exploration bear out its value proposition. In the great unknown are rich deposits of metals that one can discover, delineate, and sell, or mine to generate profits many 10’s, 100’s or even 1000’s of times greater than the money invested to discover them. Pretty easy but…. the likelihood of success is minimal. We have all heard…

The more interesting question relates to why the companies share price dropped to 2c over a year. Ultimately, I believe this was caused by a confluence of factors such as neutral sentiment towards gold, a loss of speculative money from the resources sector, negative sentiment towards Africa and finally a period during which the company was just grinding through resource drilling and not providing anything of particular excitement. Ultimately, the nearby Osino takeover was a great catalyst for WIA.

Closing remarks

I go into some details reflecting on my though processes for the discoveries that I was a part of. This is primarily to study what I did right and wrong , so that I can do much more of the former and less of the later. I generally find that going through this process I can draw out the maximum ammount of learning.

I would be keen to hear from others on how they succeeded in, or butchered their participation in a discovery.

Cheers,

CC